When you are looking for a loan or financing, you need to compare the cost of that money. The two key indicators for evaluating offers are TAN and APR: what is the difference?

See also : How to choose CBD?

TAN stands for nominal annual rate and is used to determine the payment and duration of the loan. On the other hand, APR stands for Annual Percentage Rate and includes both the interest rate and the additional costs of financing.

In addition to understanding what TAN and APR are, it is also important to know how to use them: is it true that you should always look at the APR to find the cheapest loan?

Related reading : Discover where Sri Lanka is located on the world map and its wonders

Not always, and you will find out why. You will also find here all the information you need to understand what TAN and APR mean, how they are calculated (with practical examples), the average TAN and APR in the loan market today and how to find the most affordable ones.

TAN and APR: what they are

TAN and APR are percentages in the contract and in the summary document of a loan that help compare the most profitable product.

TAN and APR tell you a bit about the cost you will incur when borrowing this money, but with one difference:

- TAN: this is the nominal annual rate, meaning the portion of interest that must be repaid on an annual basis. It is used to determine the interest rate and the duration of the loan;

- APR: this is the global effective annual rate and also takes into account all additional expenses related to a loan (survey, insurance, etc.).

If financing did not incur any additional costs outside of interest, TAN and APR would be the same. But since that is very unlikely, the APR tends to be higher than the TAN and is also the benchmark value for those evaluating a loan.

But not always.

What are TAN and APR: Video

Calculating TAN and APR

Even if the documents for financing your car, or the renovation loan, already show these indicators, calculating TAN and APR by yourself can still be useful. So, how do you do it?

How to calculate TAN

To calculate TAN, simply multiply the monthly rate(s) by the number of months (12). In fact, the calculation is done under simple capitalization.

TAN = rate * 12

Often, TAN is a determined and fixed value, which does not depend on the loan amount or the amount paid (determined arbitrarily by the financial provider).

How to calculate APR

The calculation of APR, on the other hand, starts from the nominal rate of the loan. It is necessary to calculate the interest and add it to all additional fees, such as:

- survey fees;

- compensation granted to the intermediary;

- deposit recovery fees;

- practical opening costs;

- insurance policy.

The formula for calculating APR is very complex and special software or comparators are often used to estimate the value of the global effective annual rate.

Do TAN and APR add up? APR calculation formula (Bank of Italy 2009) Is there a temptation for some to equate them or average them, but being two different indicators, TAN and APR should not be added together.

Current TAN and APR

To get an idea of the high or low level of TAN and APR offered by the financial company, it can be helpful to have a benchmark. Knowing the average value of current TAN and APR can be useful in this regard.

By comparing the best offers for personal loans online, the current average TAN is around 5.6%, while the current average APR is 6.8%.

The TAN and APR rates offered by Younited are very attractive, among the lowest interest rates available online:

- average TAN 4.6%;

- average APR: 6.6%.

Younited’s offers can often be even cheaper, with a fixed TAN of 2.66% and a fixed APR of 4.99% (excluding insurance).

Learn more about Younited

Cheaper TAN and APR: what is it about?

When evaluating the convenience of loans and financing, it is easy to create confusion between the different TAN and APR. Often, you do not have the right criteria to decide on the most profitable product, which allows you to pay more interest than you should.

Let’s start with the simplest concept. If you have a friend who works in the industry, you have probably heard this advice:

Before applying for a loan or financing, look at the APR, not the TAN.

This statement is true. In fact, without considering additional costs, TAN does not tell you everything about the real price of a loan. Some financial providers offer loans at zero rate (TAN 0), but inflate the APR to gain benefits from the operation (often modestly hidden).

Result: Even if the TAN is low or very low, the costs are there and could be higher than the alternatives.

What really matters is the global effective annual rate. But is it really the best indicator? Is financing with the lowest APR automatically the cheapest?

Some forums and financial sites often read phrases like this:

When one APR is lower than another, the final cost will certainly be cheaper.

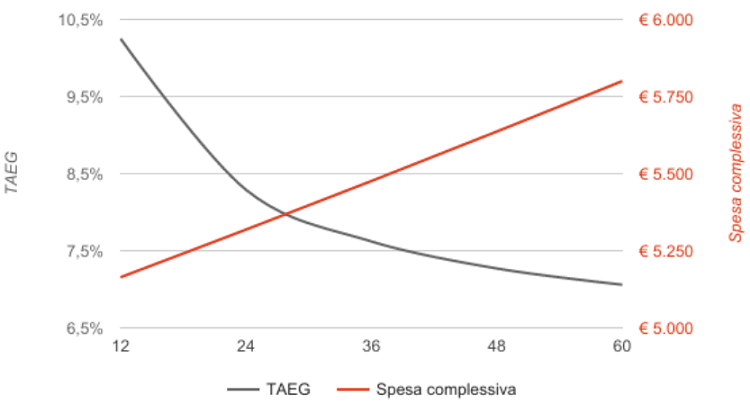

An interesting analysis from Soisy seems to say the opposite. What makes this common idea erroneous is the duration of the financing, the timeline (see the graph below) on which the return of money is developed.

Since the APR is “distributed” over the entire period taking into account the various additional costs, a loan paid over 7 years will have a lower APR than a loan of 5 (see the example below).

The reason is that most additional costs (preliminary survey, practical opening, compensation granted to the intermediary, etc.) are paid when the loan is opened.

If a loan lasts less time, it will have a higher APR, as the costs will weigh more heavily on the monthly payment. If, on the other hand, the financing is longer, the additional expenses will be spread over a longer period.

But financing that lasts more months will necessarily have higher costs. The longer the loan duration, the lower the APR, but the expenses will increase! (source: Soisy) Therefore, choosing the lowest APR is certainly not cheaper.

This paradox can create problems in some cases, and it is good to be cautious. Essentially, a loan with a very low APR is not necessarily the best.

Example of calculation with TAN and APR

Suppose we request a loan of 10,000 euros over 5 years (60 months), which involves initial opening costs and survey fees of 150 euros.

The TAN is 7.5%, while the APR is 8.17%. The calculated installment on these values is 200.38 euros per month.

We repeat the same calculation with a loan of 10,000 euros but this time to be repaid in 7 years (84 months). The TAN remains unchanged at 7.5%, but here the APR drops to 7.99%.

If we only consider the lowest APR, we should choose the second, longer loan. But in terms of total amount, which is more expensive?

| Loan Amount | APR | Duration | Monthly | Total Repaid |

| 10,000€ | 8.17% | 60 months | 200.38€ | 12,022.80€ |

| 10,000€ | 7.99% | 84 months | 153.38€ | 12,883.92€ |

Although it shows a lower APR, the second loan is actually more expensive than the first because it is longer. In fact, I will have to repay about 800 euros more in the end, which I would have saved by closing the financing earlier.

Thus, comparing APR is only useful between similar loans (same term) and not in absolute terms.

A better indicator to know if financing is profitable or not, and easier to calculate, is the total amount to be repaid. Always calculate the final cost in terms of money to be returned: this is the most basic but most effective check.

In conclusion: the most profitable financing is the shortest duration and the lowest APR.

Find loans with affordable TAN and APR

TAN and APR — Frequently Asked Questions

What are TAN and APR?

TAN and APR are two fundamental elements to understand whether financing to buy a car or anything else is practical or not. The two values have important differences that you need to know: read the guide.

What is more important: TAN or APR?

APR is certainly more important than TAN as it takes into account many additional expenses. It is useful to check the APR if you want to know the cost of financing, but there is an even more reliable value. To learn more.

What is the difference between TAN and APR?

The difference between TAN and APR is that the former (nominal annual rate) expresses the interest of the loan on an annual basis, while the latter (global effective annual rate) indicates the total cost of the loan taking into account various additional fees.

Tag: More info on CBD